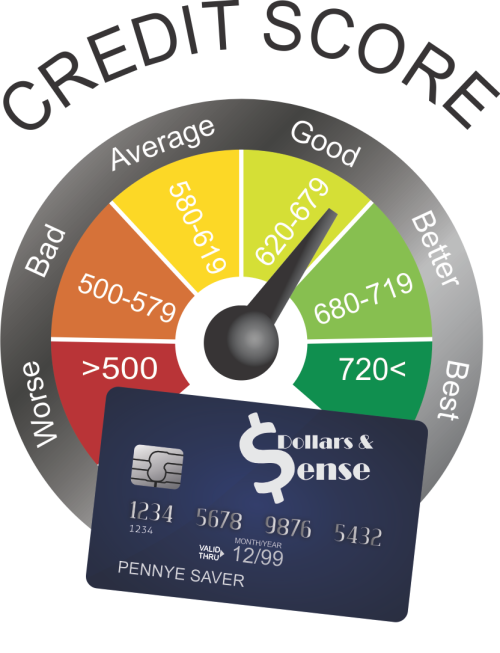

The information in your credit report is used to calculate a statistical credit score, usually ranging from 350 to 850. Credit scores help lenders decide who is most likely to repay in full and on time. This reduces the risk of losing money. Consumers with higher scores may qualify for loans with the best terms and lowest interest rates. Scores below 620 may mean higher l oan costs. To improve your score, concentrate on these points:

oan costs. To improve your score, concentrate on these points:

- Pay ALL your bills on time.

- Keep balances low on credit cards and other revolving credit.

- Use a few credit cards consistently over time, rather than switching to a new card often.

- Apply for and open new accounts only as needed.

Are you in over your head? Are you spending more than 17% of your net income on non-mortgage debt? If you are at 20%, any minor financial crisis could send you over the limit and you may begin to use credit cards to purchase everyday necessities.

Click here for more information about credit scores.

Getting out of debt takes a lot of self-discipline, but you can do it. You can solve most credit problems in two to three years if you are patient and stick to your plan until you pay all of your debts – no matter what. A plan to reduce debts gives you a sense of control. Paying a little back is better than just worrying or doing nothing. Many creditors are willing to work with you on your problems if you notify them BEFORE bills are due and have a good plan. Do not avoid creditors.

If you are serious, STOP USING CREDIT NOW. Find ways to increase income, reduce debts and create a written debt repayment plan. Remove credit cards from your wallet, make sure that they are not easily accessible and vow not to use any other form of credit except in an extreme emergency.