After writing your payment plan, it might be time to contact your creditors. Phone creditors first, explaining your situation. Be prepared to explain why you have fallen behind, your current income, and how you plan to bring this debt up to date and keep it current. Don’t wait for creditors to contact you! They will be more likely to work with you if you contact them before bills are due. Some credit card companies may ask that you ‘wait until you’re a 3-6 months behind’, which is not beneficial to the customer. This is why it is important to have your own paper trail with the creditor’s that you are working with to keep everything documented. You may also want to contact creditors in writing.

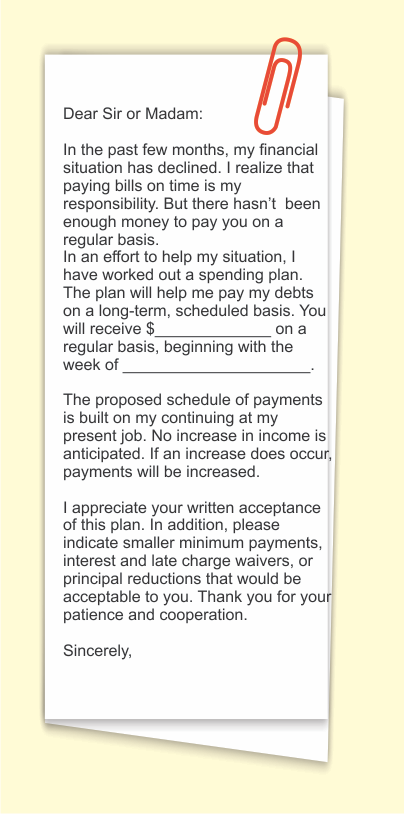

The sample letter shown is written in a way that business people recognize. Adapt the letter to your needs. Place the return address at the top of the page, list your address, your telephone number, the date and your account number. Before you make any changes in your payment plan, make sure that you receive a confirmation in writing from the company that they accept your plan. Otherwise, you could inadvertently put your account and your credit standing in jeopardy by having a charge off or settlement to your account and that negative information stays on your credit report for at least 3 years. Be sure to send the letter in a manner that you will receive a signature confirmation. Begin your own paper trail, so that you are covered in writing. This is NOT a time to do things via email, not knowing for sure who, if anyone will get back to you. Before you dispute a negative item on your credit report, understand ALL credit laws in total. Unfortunately, scam artists share half of the law and consumers end up in far worse positions.

You can download a sample Dispute Letter and Checklist here. Dispute Checklist – Dispute Letter.